Money Moves is an ongoing series on how to build a business in today’s creative landscape. Topics range from hands-on advice to broader thoughts on how to grow your empire as a freelancer or company founder/employee. If you want to see specific topics discussed, you can email us at editorial@archive.maekan.com or Slack us directly in our members-only chat.

Scott Masek is MAEKAN’s COO. Prior to joining MAEKAN, he spent over 5 years working in finance and tech across a range of positions and fields, most notably in investment banking and e-commerce.

Parents are an infinite source of wisdom. My father once told me, “You are only as good as your next deal.” He spoke from experience; in his line of work, deal making and execution are everything. I keep this piece of advice in the back of my head at all times, especially now as a business owner and executive.

Before you master your ABC mantra (Always Be Closing!), it pays to have a healthy deal pipeline. Previously, I established how you should split and categorize projects — in this article I will focus on how you can build a pipeline that achieves your goals. I will cover where your first deals will come from, how to expand from there onwards and some useful tools we use at MAEKAN.

Building a Pipeline Foundation

In our experience and based on community feedback, the vast majority of founders and entrepreneurs pen their first deals through relationships formed via word-of-mouth. In fact, many people first venture into business knowing that they have landed at least one secure client, which alleviates the stress of initial business development.

This is significant for a few reasons:

- Your network is your business card while you establish your brand’s reputation

- The people closest to you will take the time to understand your offering, helping you edit your pitch and product

- Working with established connections gives you a safety net and a sandbox environment to experiment within

However, if you find yourself overpromising and under-delivering, even to friends, you’ll definitely hurt your reputation, which is particularly damaging in the early stages of your endeavor. You should treat those first, close customers with even more care than subsequent connections.

The great Warren Buffett said it best, “It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.”

How many deals should you have to begin with? There is no correct answer because it ultimately depends on cash-flow. If one client can pay the bills for a whole year, then that’s enough to get started (and gives you time to find new ones).

However, if your first project is both short and cheap, you’ll either need to have certainty over your next few deals, or put your new venture on hold. Make a list of all your confirmed clients and deals that are almost certain to close and plan ahead before you embark on your journey.

Depending on your work nature (project-based, cyclical), you’ll need to assess how early you need visibility for your pipeline. If your skills are in demand, you can get away with locking down deals a little later (a few days or couple weeks before in-progress contracts expire). If you are a bit more niche, leave yourself plenty of time to avoid any bad surprises.

Your first deals are crucial for your pipeline. When you are starting from scratch, these initial projects create immediate projections of your business’ future cash intake and workload. Having a firm base is just the launchpad for sourcing more opportunities.

Where to Go Looking

Landing your first deal may be an easy feat, but hunting for your first non-aided deal is a whole new challenge. Corporations hire massive sales teams to handle this type of work, cold calling potential clients to acquire their business. If you are a small business or single individual, you will need to seek out deals on your own.

To begin, you should solidify your understanding of: i) what you are selling, ii) why you are selling it and iii) to whom you are selling it to. Entrepreneurs often lose track of all three facets and waste energy chasing the wrong clients.

If you are offering a service where switching costs are high for a prospective client (e.g: the time and effort to change from platform A to platform B), you’ll likely run your efforts to the ground unless you can demonstrate significant upside. Understanding your product, scoping out your market diligently, and finding quick wins will drive your business’ growth and increase your confidence in being able to close more complex deals in the future.

Look to develop your business in the following three key areas:

- Word-of-mouth/recommendations: Opportunities that arise from word-of-mouth will always be a strong source of new deals because they rely on a prior client’s positive experience of your work. These deals will often be of higher quality because your prospective clients have used a trusted third party to vet your services.

Closing these deals becomes a byproduct of your superior service offering. Leverage your network as your former clients and peers can offer warm introductions to otherwise inaccessible people. This speeds up your sales for your product/services.

- Circle of competence: You’ll spend the bulk of your time making circle of competence deals. By looking at companies, individuals and potential partners in your industry, you’ll be able to assess what a prospective client may be looking for in a service provider and pitch them.

Think of these opportunities as “N+1”, where “N” are your primary customers/relationships and “+1” is the circle one step beyond that, consisting of slightly different client types looking for similar work. Opportunities within your circle of competence can require some cold calling, but you can often get the necessary access through your extended network.

This is a great zone for you to expand your thinking as to how your work can make sense for a potential partner that may not know they need your services.

- Stretch opportunities: Stretch opportunities require copious amounts of cold calling and pure luck. Moonshots are meant to be hard—you’ll send a hundred emails to potential stretch clients and get fewer than five responses, all negative most likely.

As the name suggests, you don’t look for these deals expecting to close the majority of them, but you also know that landing just one will tremendously benefit your business.

In attempting to reach these clients, you should spend more time crafting your approach to improve your chances.

Experimenting with imaginative ideas outside your area of expertise is valuable even as an internal exercise. What does a MAEKAN Netflix show look like? What is the MAEKAN Fisherman Friend’s flavor? How would MAEKAN redesign buildings? The possibilities that emerge are exciting, and a properly tuned pitch could land the meeting that leads to a moonshot deal.

If you were to break down your time over these three kinds of deal sources, I personally feel that it should be divided 35/50/15. If you take 10 hours in a week to deal hunt (this can be a little or a lot depending on your setup), then you could use this split to optimize your time. You’ll need to figure out which split works best for you in light of your network and available time.

As you can see, I believe that circle of competence deals are the most important, because this is where you can truly test your business and develop your acumen and salesmanship. More importantly, you can and should be able to charge more for that kind of project because no one is asking for a “homies rate” for your work. It’s harder to say no to a friend for a discount than for someone you only know in a professional capacity. Don’t allow yourself to work for cheaper than what your value is. Someone will always be willing to pay if you are fair.

The 15% time spent on moonshots should be on hyper-crafted pitches to clients you really want to work with. Take that 15% of time to focus on just one or two clients. Since you expect to get little to no responses, give it your best shot but don’t waste too much time. Think of it as a passion project: even if it doesn’t lead to anything, you’ll feel glad that you tried and learned from the experience.

In the context of deal making, especially for stretch opportunities, you become vulnerable. Some creatives are shy about self-promotion, thinking that constantly pitching their work could hurt their image or work quality.

Good work does speak for itself, but as we mentioned when discussing pricing strategies, only to a degree, since free-markets and paid advertising have made the overall landscape noisy and flat. While you build your deal pipeline with more client types, you’ll face more adversity in the form of questioning and challenges from prospective partners. As is often the case, the key is to adapt and press on.

Don’t continue sending the same email to different people, but instead find ways to best frame the value you bring to a prospective client, then pitch that as only the best promoter and advocate of your work can. Ultimately, no one knows your business and your value better than you.

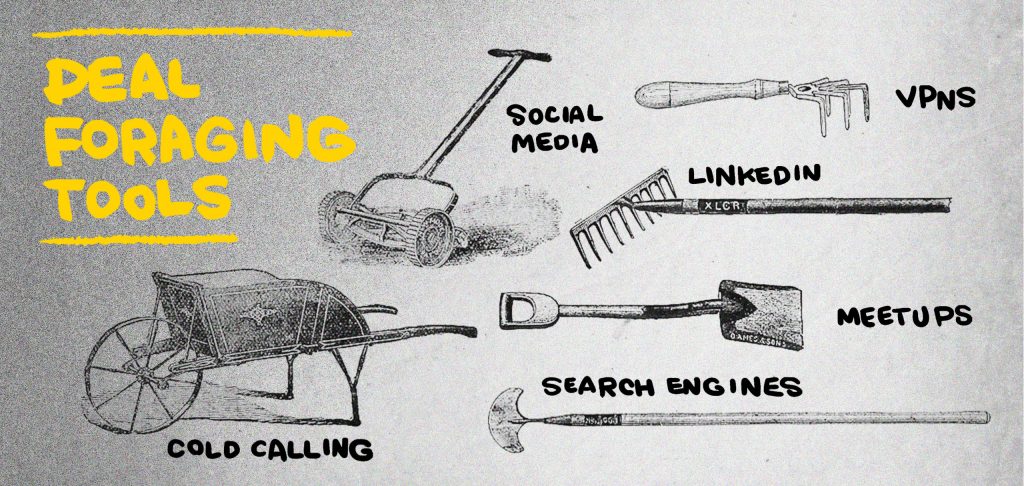

Deal Foraging Tools

At MAEKAN, we use a combination of tools to source our deals, all of which are readily available to you both online and offline. This list is more geared towards traditional businesses and is non-exhaustive, but it will give you an idea of possible resources appropriate for you to hunt with.

- Instagram/Social Media: Absolute shocker! Social media is both an acceptable place to reach out to prospective clients but also signals openness to being approached for potential partnerships. If your business venture has a social media presence, use those accounts to make connections. Bear in mind that while your account is still young, its size may negatively affect your success rate of getting responses.

Since reaching out on social media means that potential clients will judge you based off of your accounts, consider what they look like and how they might attract a certain crowd. Lastly, use different account types to find different kinds of clients. The people/brands most active on Instagram may not be the same as those on Twitter. We recommend understanding the landscape in depth to maximize your upside. - Search Engines / Optimized Browsers: Optimizing the results Google gives you by tweaking the search inputs (e.g, relevance and time stamps) will save you time in getting the answers you need. When you have unfruitful searches, try using alternative terms/targets to get to your end point. For example, you may not find a CEO’s email, but you might find the email of someone in their company’s senior management; the email format within firms tends to be the same across the board.

Most web browsers allow you to add plugins, some of which are helpful in finding potential leads and getting insights. I personally use Skrapp.io for emails; it’s not perfect, but it gets me a foot in the door fairly regularly. - LinkedIn: In today’s business world, LinkedIn is a necessary evil. As you grow your network on it, you can see who is within your immediate reach or one or two degrees of separation from yourself. In addition, you can search for firms by name or industry and get a breakdown of employees currently working there, helping you know which person is the most appropriate to send your pitch to.

- VPNs: A good VPN helps protect your IP and identity online. I find this useful when using Linkedin to avoid hitting the free versions’ search limits. A new IP helps me go back to square one so I can keep finding more names. VPNs are also useful in combination with your browser for localizing search results.

Because your search engine relies on your IP address, switching to your location of choice helps you make sure results are relevant to the place you are interested in. Getting solid results on New York pizza parlours is easier with a New York IP than one from Berlin. - Meet-ups/Conferences: Conferences and meet-ups reliably result in new leads. Some events can be expensive, but there are many you can get invited to or are entirely free. Seek out local opportunities and cast a wide net when it comes to venue and type.

Great opportunities are not all obvious, so be adventurous in your meetup endeavours! The hardest part is being opened to meet people, and do so efficiently. This can be taxing for some people: make sure you are in the right frame of mind to make it worth your time. - Cold Calling: Oh dear, you mean, actually using a phone… to call someone? I’ve gotten lucky in the past when calling a hotline and asking for a person directly. Identify specific individuals you want to reach and prepare a script so you’re not caught off guard by assistants, automatic redirects, or other surprises.

If you’ve never tried cold calling, giving it a go and not landing a deal will still improve your speaking skills. Most people no longer make calls, so you optimize your chances by going the old school route.

On the topic of scripts, it’s good to have a game plan. Typically, you’d want to know exactly who you need to speak to and why. If you are locating a department, explain why you are calling to begin with.

If you find that your counterpart on the other end isn’t cooperating, you should either ask for a phone number or an email you can reach out to. If the person is “not at their desk,” ask when they will return, or when is convenient to call back. Always remember to be polite, but direct and firm.

How to Track Deals

In small teams, you tend to do everything you need to do, rather than what you want to do. Staying focused becomes difficult when problems keep popping up, which is why you need help keeping track of incoming deals and potential leads. A Customer Relationship Management (“CRM”) System, if used properly, keeps the relevant information in one place and reminds you when to send follow-ups, create pitches, and finalize deals.

Regardless of what system you use, we recommend the following when tracking your ongoing pipeline:

Organize clients by time and importance. If you are using a Kanban/Kaizen system, put the most important things at the top so they come to mind most rapidly.

Limit the amount of columns on a given surface/screen so you can quickly visualize everything. This lightens your cognitive load when you do your checks.

Systematically input core details after every interaction. Many CRMs can sync directly with your email, or you can use mobile apps to input the details on the go. This is the hardest, but most rewarding part of the tracking process.

When you recall something, but don’t remember the exact details, you should be able to find them all in your tracker.

Set reminders and automate. For first time contacts, set reminders or auto emails to follow up after your first touch point. Most people don’t respond on the first email, so set a follow up for three to seven days after your first follow up to keep the lead warm.

Keep your workflow clean. If strangers were to look at your system, they should be able to understand it and add to it. This is crucial as your team grows, so standardize as much as you can.

Respond promptly. We prefer to revert within a 24 hour window. If the response requires work that takes more than 24 hours, you can send a short response that explains when clients can expect something more in depth from you in a given timeline.

If you can maintain consistency, your pipeline will remain up to date and you’ll also showcase professionalism in the process, which is crucial when you are starting out.

Good vs. Bad Pipelines

You now know how to seek out new deals, track them, and close them. However, one looming question remains: is my pipeline strong enough to move forward with clear, quantifiable certainty? No one wants to spend six months working on potential deals with flaky people that can’t make a decision or are just taking you for a ride. There are a few ways to distinguish between a good and a bad pipeline, utilizing your honest discernment and some artistry in the process.

Goal measuring

- You can track your pipeline based on goals you set. If you have a number of deals or a deal value in mind, you can assess if your pipeline will help you reach your weekly/monthly/quarterly/yearly goal within the specified timeframe.

However, just because you have a lot of potential contacts lined up doesn’t mean that you are anywhere closer to reaching that goal. You need to determine the stage each conversation is in and the likelihood of deals converting. - Are prospective consumers/clients answering regularly? Are they asking questions? Are they engaged? Have you spoken on the phone more than once? Have you discussed their pricing expectations or not? As a rule of thumb, the more direct contact you have had, the better the odds are of a deal being struck, though the contact does need to create increasingly forward momentum.

- If you think you have enough potential clients that will yield the necessary results to reach your targets, then you have a healthy pipeline that you should continually expand and build upon. None of the pipeline matters if you don’t close anything.

- A word of warning: if you have one good client that covers your year, it can be a blessing but also a liability. You should always look to spread your risk over a few clients. For example, your top five clients should not yield more than 50% of potential revenues. Adjust those numbers according to your industry, but keep this ratio in mind as a rule of thumb.

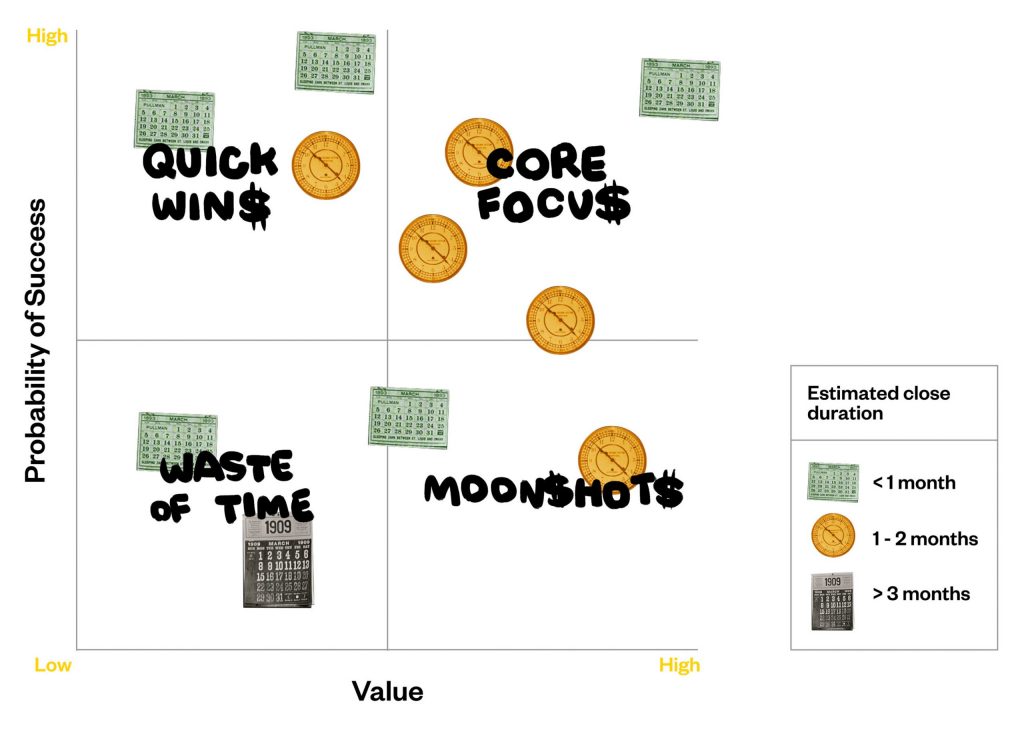

Probabilistic Measuring

- Probabilities are a good way of measuring a pipeline’s value. For every client and interaction you have, try to assign a probability of success and a project value.

Early interactions would yield low probabilities, while discussions further down the line would be marked as higher probabilities. Be sure to update the figures as you go along.

- Based on these probabilities of conversion, you can then model what your pipeline will look like within the forecast period. You can estimate with some certainty what your cash flow will look like. Doing so will give you a clear sense of how likely you are to stay in business and what leads you need to focus on, which to cut, and when to seek fresh ones.

- For example, a stretch client that you’ve had an email response from may have a 10% chance of working out at an estimated budget of $50,000. Another project on which you’ve been working on for 3 months may have an 85% chance of closing for $15,000.

You can also put a full 0% chance on a client you’ve been dealing with for months who never responds in a timely fashion. At this point, it’s sunk cost—don’t waste any more time on it. Only you can, as objectively as possible, assess where the deals will go, and if you are close to closing them or not.

Being negative yields better results than being overly optimistic. Optimize for bad surprises rather than good ones when forecasting your future pipeline results.

- As is the case when measuring via goals, you’ll want to ensure you spread your risk and workload across timelines and projects. If you see that most of your pipeline is likely to close and begin within a month, then you’ll need to plan ahead for new clients before you start, especially if the projects are resource intensive.

Try to blend both methodologies, using goal setting and probabilistic forecasting to set a base, worst case, and best case for your pipeline.

We typically expect a client perusal life cycle to range from a few weeks to a few months. We are happy to take more time pursuing larger clients, but we do so knowing that the payout for our efforts and patience will be greater.

If many small potential projects are taking up all of your pipeline building time, you’ve got a problem. Your pipeline won’t wind up justifying the time and effort you spent. On the flip side, if you only close a few big clients, you are at the mercy of the next economic cycle which can crush your business. As a company, you are part of a larger ecosystem, which means you must prepare for everything that could come your way.

A healthy pipeline mixes and matches projects of all sizes and operates with appropriate deal cycles. Don’t wait six months to close a $2,000 deal. Always assume that larger or more interesting opportunities take more time to close, but don’t ever offer your time for free in wooing noncommittal prospective clients.

When the Taps Run Dry

The hardest part of maintaining a deal pipeline is when it begins to slow and dry up. It’s important to understand the root cause of this problem in order to best assess how to fix it. We generally ask ourselves the following questions, which can be split into internal and external focuses.

The split and answers you provide based on your dry patch are a reflection of your honest assessment. If you notice that competitors are thriving but pinpoint your woes on external economic circumstances, then chances are you have not taken a hard look at your product or sales process.

External factors are external by nature, meaning that they are almost entirely out of your control. If you run into a drought because of such factors, then it means you’ll need to look elsewhere beyond your current field of expertise to tap into new opportunities. This may entail taking on some client work you wouldn’t previously consider; note that this is temporary and that you’ll re-adjust once conditions are more clement.

On the contrary, if your answers find internal weaknesses, it means you need to fully re-assess your current setup and scope of work. What do you think is causing this problem? How do you test this?

How do you validate your findings? Sometimes, all it takes is a phone call to a prospective client to find out why you didn’t get a deal. Not all clients will offer feedback, but most are happy to have a conversation with you so you can finetune your pitch.

They stand to gain from helping you if you provide better services to them down the road. The hardest part of internal problem solving is being fully honest and transparent with yourself. If you are unable to do so, ask a third party you trust to provide you with the feedback you need to push forward.

In periods of drought, the impetus is always on speed because your cash flow dries up extremely fast. Figure out how to get some quick wins under your belt, no matter how small, to keep your store front open until you are fully back in the game.

Close Deals, Open Relationships

Deal pipelines are the lifeblood of your company or your wellbeing as a freelancer. Whether you are fresh into your venture or a seasoned veteran, there will always be a need for you to source opportunities as you move forward.

If you do so correctly, you’ll gain a loyal customer base to support your business as it grows; repeat business is always optimal to keep track of long-term cash flow. However, during tougher periods, asking the right questions and seeking optimal answers will ensure that you progress accordingly.

Lastly, once you get in the habit of things, you’ll always find yourself deal hunting. A casual dinner can open up conversations that generate more ideas and potential projects, so be sure to keep your business cards on you at all times.

From experience, great business is always organic, which is why we seek genuine connections first, which may turn into opportunities down the road. Clients hear pitches all the time—we use this as our motivation to be different, because, for the most part, we wouldn’t work on a deal we had no interest in to begin with. Share your passion with others, as this will open up more doors down the road.

To part with some additional wisdom, the author Patricia Fripp notes, “To build a long-term, successful enterprise, when you don’t close a sale, open a relationship.”

Grow further!